Key messages

- The stage has been set for a paradigm shift in the US small business insurance market, thanks to heightened buyer awareness driven by coverage gaps exposed during the pandemic as well as preferences for more policy flexibility, along with the emergence of InsurTechs and other alternative providers.

- Legacy insurers still offering commoditized policies that are sold primarily on price through traditional agents and brokers should therefore consider reinventing their value proposition and business model, while those who have already launched transformation initiatives may want to accelerate such strategies.

- Insurers have an opportunity to capitalize on enhanced attention and higher trust levels among small-business buyers to grow the overall pie and their own market share by developing more customized, adjustable coverages and enhanced advisory services, marketed through a wider variety of channels.

- Since meeting expectations for “cover plus” packages offering concierge service via individual agents and customer service representatives is probably not economically viable for most providers, insurers should be looking to expand online, do-it-yourself capabilities—from automated risk management training to robo advisors.

- With the rising threat of disintermediation in an increasingly diversified, online economy, legacy insurers should be bolstering the digital capabilities of their agency force while exploring supplemental platforms and partnerships.

Shifting customer needs, preferences setting the stage for major shifts in small-business insurance

While the pandemic may have made many small businesses keenly aware of potential shortcomings in their insurance portfolios, filling the gaps by simply selling them more coverage could provide a temporary bump in premium volume but isn’t likely to sustain short-term retention or fuel long-term growth, a Deloitte Global consumer survey has revealed.

Instead, many small-business respondents are also seeking more diverse and comprehensive solutions than what has traditionally been offered in commoditized risk-transfer policies. Significant segments want greater coverage and pricing flexibility, additional risk management services, as well as new sources of insurance, the survey found. While this article focuses on the 501 US small-business owners responding to the survey (see more US respondent results summarized here), these sentiments and trends were largely echoed by the 5,300 respondents from 14 countries (see sidebar, “About the survey,” to learn more about our methodology).

In light of these findings, most small business carriers might need to consider reinventing many existing products, launching new types of insurance for emerging risks, expanding distribution options, and bolstering service capabilities rather than continuing to compete and differentiate mainly on price and coverage levels.

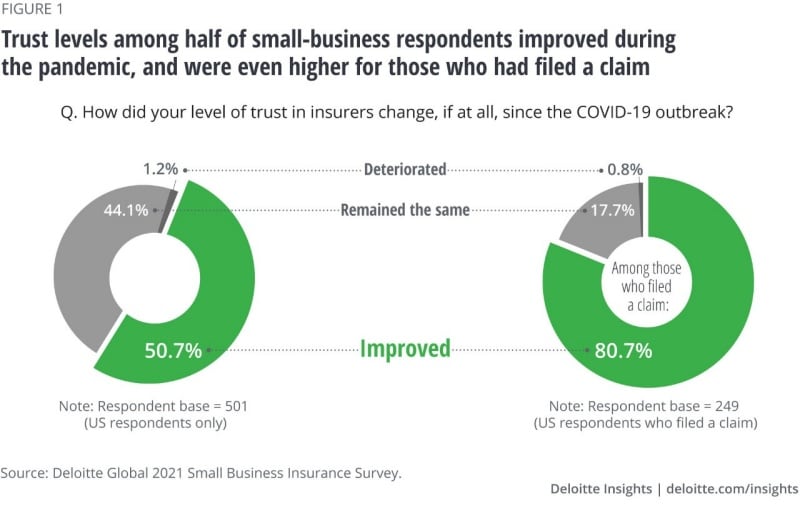

If the stage has indeed been set for a significant paradigm shift in the small business market, legacy insurers could be well-positioned to pivot to new business models as trust levels among respondents rose during the COVID-19 outbreak—especially among those who had filed a claim (figure 1).

The main reasons cited by respondents for the rise in trust include premium reductions provided while businesses had to close, advice offered by insurers on how to cope with the implications of COVID-19, as well as accelerated claims payments.

However, trust levels will likely wane over time if insurers do not pay heed to shifting small business customer needs and preferences. Deloitte Global’s survey identified several potential vulnerabilities for legacy carriers—any one of which could undermine their ability to compete against cutting-edge InsurTechs and a widening variety of nontraditional players from outside the industry. This article will discuss options that insurers might consider for adapting to this changing landscape.

New and enhanced products could help insurers grow the small-business market

In the pandemic’s wake, Deloitte Global’s survey detected greater concern among a significant segment of small businesses about the adequacy of their insurance in terms of how much coverage they have, emerging exposures to address, and a lack of policy flexibility.

At a minimum, carriers and their intermediaries should seize the moment and consider upselling existing customers by raising coverage levels for those worried about being underinsured. This alone could satisfy one-third of respondents who indicated a willingness to buy more coverage.

However, insurers may have an even bigger opportunity to grow the overall pie by marketing additional coverages for emerging risks. As the threat landscape for small businesses expands, the survey found many respondents worried about being exposed to new types of losses than what’s normally covered by traditional policies. For example, respondents showed the most concern about rising cyber risks in an increasingly digital economy, and as a result, many are more open to buying stand-alone cyber insurance coverage.

At the same time, pandemic-related lockdowns spurred greater interest in business interruption coverage, along with the idea of “work from home” policies covering business-related liabilities, equipment, worker injuries, and data security. Coverage for such risks usually apply to people who own and run a business out of their homes, such as “Working From Home Insurance” offered by AXA UK. But those with brick-and-mortar offices who have remote employees working part- or full-time will likely need more flexible terms or a brand-new policy.

Such coverage could also appeal to gig workers serving as independent contractors out of their personal properties—such as insurance offered to Uber drivers that kicks in when they’re working, defaulting to their own personal auto insurance when they’re offline.

More flexible products should improve affordability and meet shifting buyer needs

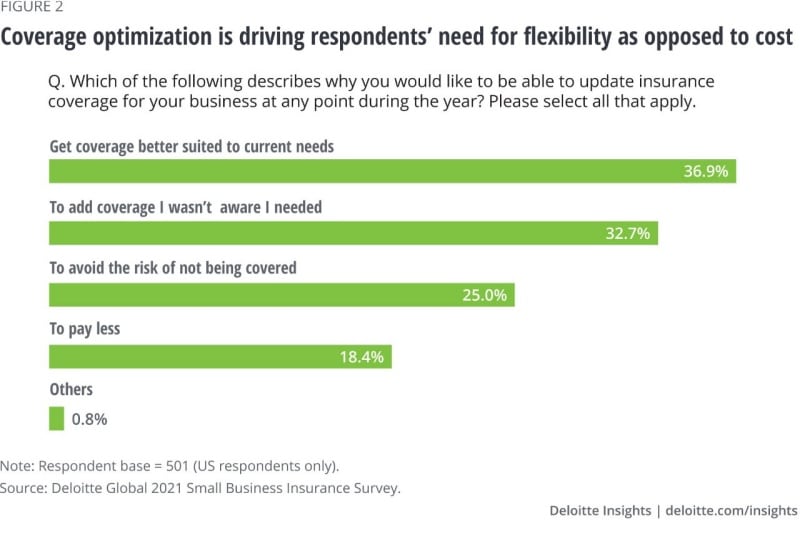

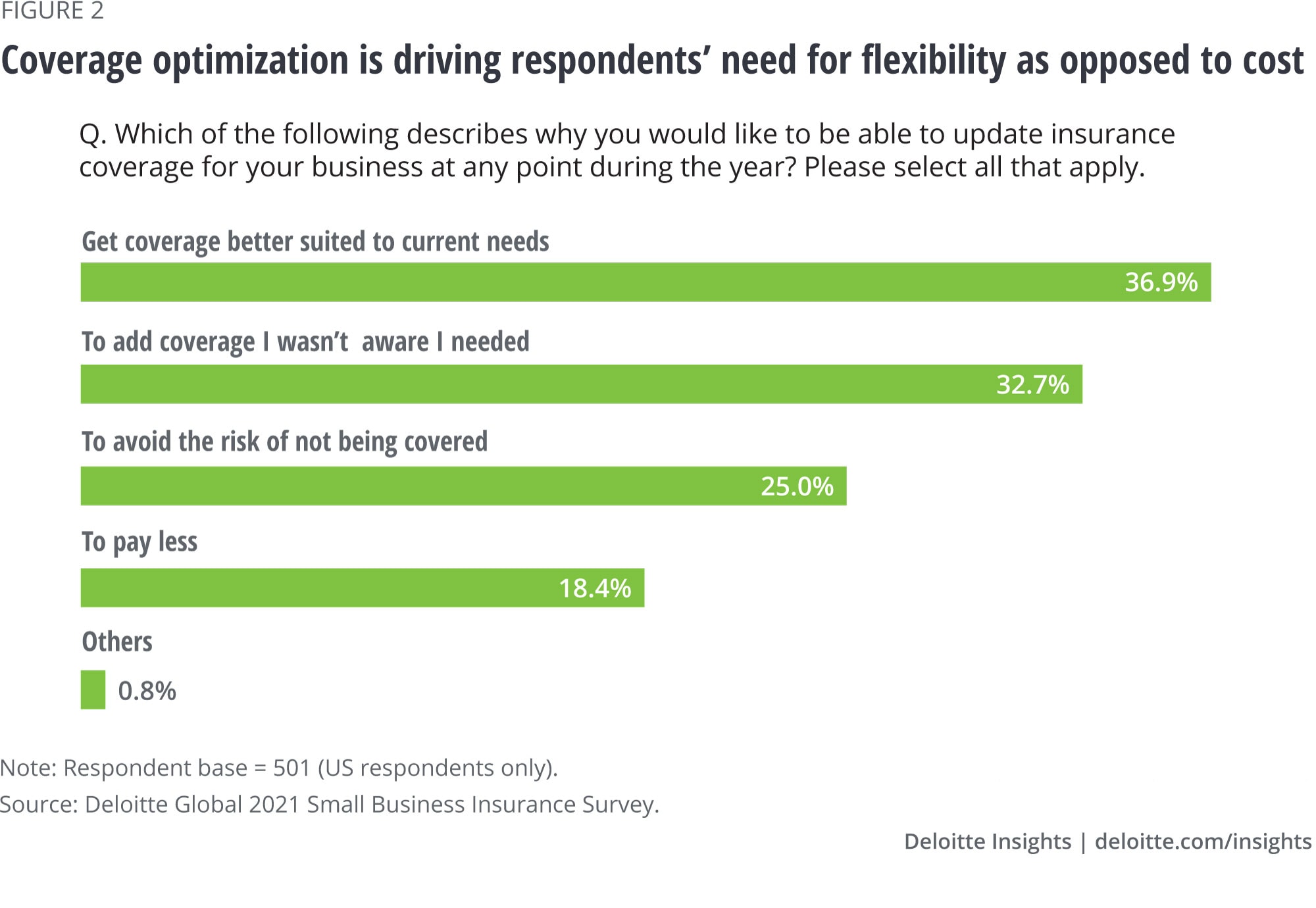

Given the uncertain nature of business conditions during and perhaps long after the pandemic, many respondents indicated that annual reviews and onetime coverage adjustments may no longer be a feasible model. Nearly two-thirds feel they should be able to alter coverage and premium charges throughout the year as conditions change. However, the top reasons for seeking such flexibility were not cost-focused as only about one in five said they were simply looking “to pay less.” Instead, respondents were more interested in optimizing their coverage (figure 2).

One example is being able to turn off coverage during down periods, such as pay-as-you-go workers’ compensation policies, like the one offered by The Hartford. Such coverage can be adjusted when small businesses lay off workers, as was done during COVID-19–related shutdowns, or hit a seasonal lull. Policies could also be shorter-term, with nearly half of respondents indicating they would rather pay a variable monthly fee based on insured asset usage.

Beyond flexibility, insurers might improve their market position by bundling more commercial coverages and providing discounts in return, as is commonly done in the US personal lines market. Auto and homeowner writers such as State Farm and Progressive are among those already offering coverage combination advantages with their small business customers as they do with their personal-line policyholders. This can save money for buyers while enhancing retention prospects.

Adding parametric triggers to policies is another option, streamlining the claims process by automatically paying out when a major event such as a flood or windstorm occurs in a designated area. One example is Zurich North America’s Construction Weather Parametric Insurance for project owners and contactors, with claims paid based on predetermined weather events without requiring proof of physical loss.

How might insurers enhance product value?

- Reinvent existing policies to create greater flexibility in coverage, premium payments, and payment triggers.

- Grow the overall pie by offering additional policies to cover emerging exposures—such as cyber, remote workers, climate risk, and use of cryptocurrency.

- Bundle more coverages to enhance convenience and lower consolidated insurance costs while bolstering chances for retention.

Holistic risk management could differentiate insurers in a commoditized market

Deloitte Global’s survey indicates that many respondents are interested in supplementing policies with value-added services. This should create opportunities to differentiate by offering customized, holistic risk management approaches rather than basic, commoditized risk-transfer policies.

However, providing additional advisory services could be problematic financially, given the relatively modest premiums and sales commissions small businesses usually pay. How then might insurers make a “cover plus” program commercially viable?

Developing more automated, do-it-yourself services could help fill the gap. Robo advisors can be programmed to explain basic coverage terms and conditions, review adequacy of deductibles and limits, and check on a claim’s status. They could also help small businesses identify potential exposures that may call for endorsements to bolster existing policies or suggest additional coverage purchases.

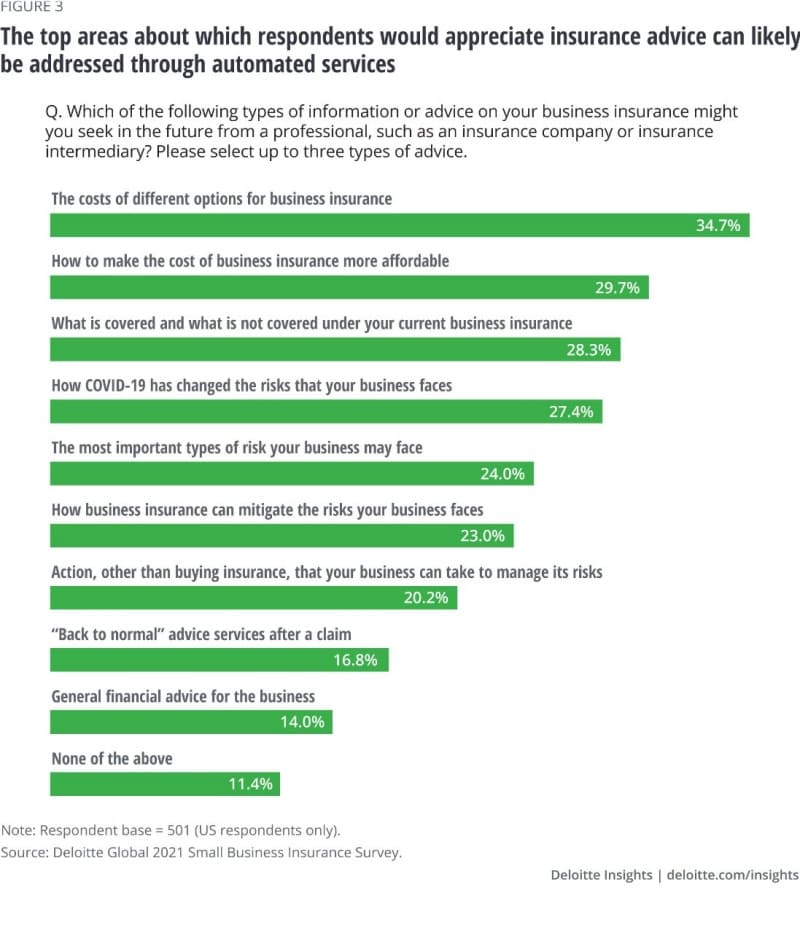

Such automated support—common for smaller-asset customers at investment management firms—is already being provided to personal-line insurance consumers through a variety of vendors, including EchoSage, offering policy reviews via artificial intelligence and machine learning. The top four areas for which respondents said they are likely to seek insurer advice are fairly basic and should lend themselves to automated self-service (figure 3).

However, Deloitte Global’s survey also found many respondents eager for guidance in tackling more complex challenges, such as cybersecurity, systemic risks, and legal issues. In such cases, insurers and agents may be able to charge added fees for risk management services. But, since small-business budgets are often very limited, automation may still be a viable alternative.

For instance, policyholders could be offered online, interactive, industry-specific cybersecurity training programs, which would benefit insurers and buyers by limiting losses. Such programs could be produced by insurers or vendors, then offered directly to policyholders or provided through agents. One example is CyberAcuView, a cyber risk mitigation company created by a group of leading cyber insurers.

Another alternative is a hybrid model, with robo self-service supplemented by video conferences or instant messaging with a live advisor—following the example of investment management firms such as Ellevest,10 Facet Wealth, and many others supporting individual investors.

Overcoming obstacles to self-service adoption

One possible hurdle to widespread use of online self-service is the desire by most small-business insureds surveyed to deal with a live person rather than a chatbot or some other automated encounter. Three-quarters of respondents would prefer in-person or telephone contact—at least when it comes to insurance sales.

To overcome resistance to automated interactions, insurers could provide an online onboarding tool at the point of sale to make policyholders aware of all the services available via the insurer’s website or smart phone app, while emphasizing the simplicity and ease of navigation when using automated tools. They might also provide gamification incentives where regulations permit—scoring points that could earn them premium reductions for completing online risk management courses, documenting suggested loss-control steps, and/or exceeding peer safety benchmarks.

Insurers could also add value by remaining digitally engaged with policyholders throughout the year, rather than connecting only at transactional points such as the initial application, renewal billing, or when claims are filed. Supplementing policies with risk management e-newsletters, texts offering safety tips or storm alerts, sharing case studies of successful loss-control initiatives, along with ongoing digital marketing of self-service options and their benefits could keep insurance front of mind and provide additional benefits throughout a policy year.

One example is Nationwide’s business solutions center, which provides a variety of information on recovery from COVID-19–related issues, cybersecurity, and resiliency, along with additional noninsurance tips ranging from managing cash flow to online strategies.

Ultimately, however, buyers should also have an easily accessible human default option, enabling video, chat, or phone contact with a live customer service representative from the insurer or agent if robo advisors and self-help online instruction alone don’t suffice. This is likely to be especially important in moments that matter most to an insurer’s reputation—such as when claims problems arise.

How might insurers enable more value-added self-services?

- Go the robo route, making customized services viable after a policy is sold by providing digital tools to help small businesses manage their insurance portfolio, file and follow-up on claims, and improve risk management.

- Keep automated tools simple and convenient to locate, navigate, and integrate via apps and a user-friendly online portal.

- Engage digitally throughout the year by offering push/pull loss-control programs and premium-saving incentives.

- Make human support readily available if problems or more complicated questions arise.

Rise of alternative channels should prompt insurers to bolster agency force, diversify distribution

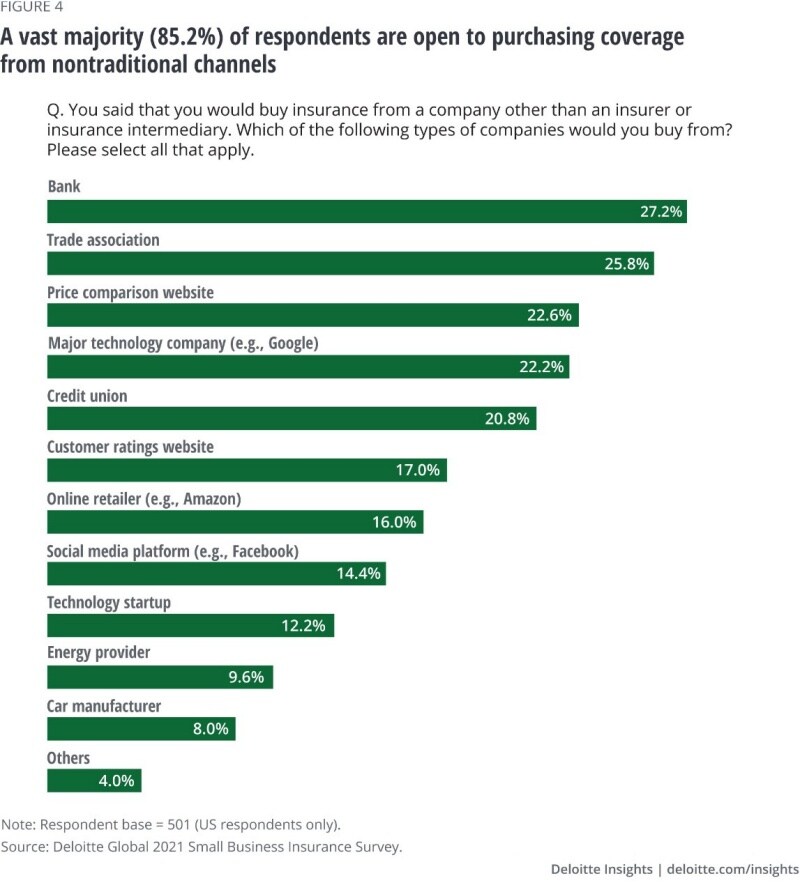

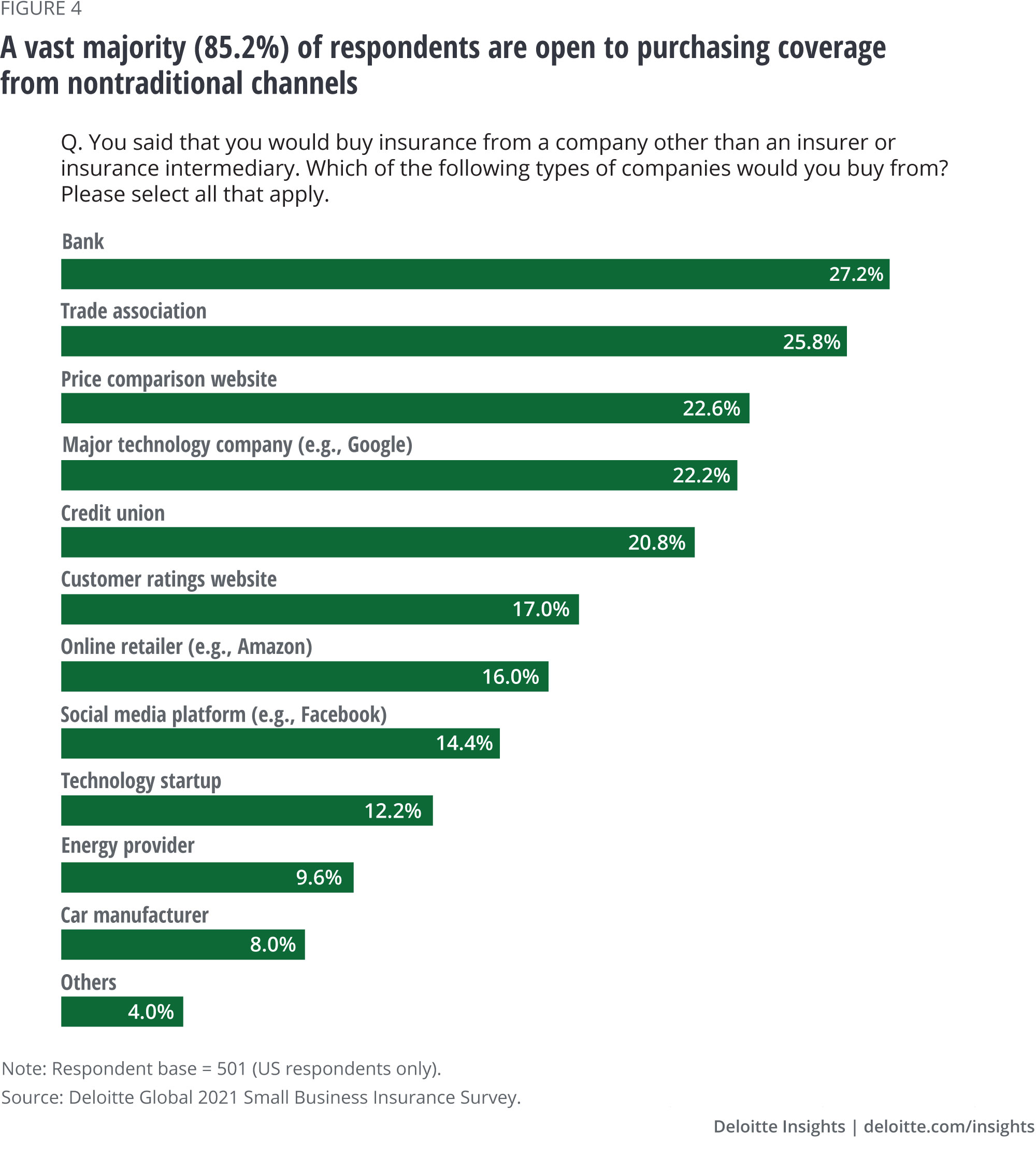

While an overwhelming majority of respondents, regardless of age, still buy through an agent or broker, Deloitte Global’s survey raised red flags about the staying power of the traditional small business insurance distribution system for many buyers. The fact that 85% of those surveyed indicated willingness to purchase insurance from nontraditional providers could leave insurers vulnerable to deteriorating renewal rates and shrinking market share as they face off against emerging competitors selling through a wider array of channels.

Some, such as InsurTechs, may simply offer more technologically advanced and convenient sales and service capabilities. Others outside the industry—such as online retailers, manufacturers, and tech companies—may seek to broaden their relationship with the small business segment by selling insurance or even embedding coverage into their own products and services. For example, Tesla launched its first auto insurance product in California in 2019, before introducing similar products in Arizona, Illinois, Ohio, and Texas.

In any case, these findings should prompt legacy insurers to reconsider overdependence on traditional intermediaries. A two-pronged strategy might help carriers maintain the relevancy of their existing distribution force while expanding accessibility via diversification. This would entail fortifying the capabilities of current agents and brokers, while at the same time establishing new digital platforms and partnerships, with both steps designed to enhance customer experience.

Bolstering capabilities of legacy distributors

To avoid disintermediation, insurers should begin reinventing the value proposition offered through their agent/broker network. Rather than relying solely on longtime distributors for price- and coverage-focused sales of commoditized products, they could consider repositioning their legacy representatives as risk managers for small businesses. Agents should be prepared to educate and advise small businesses about emerging exposures along with more innovative product and service offerings to address them, calling for sophisticated expertise.

Carriers can also help agents bolster their digital capabilities to relieve some of the agency’s manual workload and offer buyers more convenient access to information and services. Such efforts could make it more economically viable for intermediaries to offer value-added advice and service on coverage concerns, risk management challenges, and claims issues. Along these lines, Liberty Mutual recently transitioned their exclusive agent operation to an agency model to enable more specialized advice to be provided to both personal lines and small business policyholders.

Insurers could facilitate this transition with training, technology, and financial support. For example, Coterie Insurance is an InsurTech that provided scholarships last year to independent agents seeking Certified Insurance Counselor or Certified Insurance Service Representative designations.

Supplemental platforms/partnerships can expand the playing field

Since so many survey respondents were open to buying from a variety of nontraditional sources (figure 4)—whether to get a discount, to work with a provider that knows their business better than their insurer, or to receive proactive notifications for risk mitigation—more small business carriers should consider hedging their distribution bets. Some might choose to develop intuitive, user-friendly, direct-to-consumer platforms of their own, while others could seek alliances with established web aggregators, online agencies, and noninsurance players.

Symbiotic partnerships could enhance accessibility for small business buyers, hastening transformation of the distribution value chain into a holistic, omnichannel network. This approach is well underway in the personal insurance space—such as The Hartford’s longtime agreement to market home and auto coverage through the American Association of Retired Persons.

Similar strategies have already begun to be deployed in the small business market. For example, U.S. Bank deposit and credit card products and services are being offered to State Farm small business insurance customers, while giving policyholders access to the bank’s branches, ATMs, and digital banking tools.

Meanwhile, Amazon is working with Marsh to offer product liability coverage via a variety of legacy insurers to those selling goods on its online platform, along with a separate arrangement to sell coverage directly for Next Insurance, a small business InsurTech. And Chubb has established its Studio program, designed to simplify and streamline global distribution of both personal lines and small business coverage through partner digital channels.

How might insurers reinvent the distribution value chain?

- Bolster legacy sales force capabilities through enhanced risk management expertise, broader product offerings, and expanded digital services.

- Launch proprietary digital platforms or partner with online agencies and aggregator sites to diversify customer engagement opportunities.

- Explore collaboration with nontraditional players to establish omnichannel distribution.

Insurers should be pivoting to thrive in a changing small-business market

Shifting customer preferences revealed in Deloitte Global’s survey are likely to increasingly challenge insurers to become pioneers or at least fast followers in policy innovation, added-value service delivery, and distribution diversification. Indeed, how proactive and effective legacy carriers are at reinventing themselves could be the determining factor in whether their top and bottom lines shrink or grow.

Insurers should be guided in this reevaluation by the voice of the small business consumer. Those responding to Deloitte Global’s survey, both in the United States and around the world, were consistent in their calls for insurers and intermediaries to offer more than just standard risk-transfer policies that only come into play after a loss. Several legacy carriers, InsurTechs, and nontraditional providers have already begun offering more flexible policies, self-service support, and wider distribution options.

How proactive and effective legacy carriers are at reinventing themselves could be the determining factor in whether their top and bottom lines shrink or grow.

Unlike their large commercial counterparts, few, if any, small businesses have full-time risk managers on staff to anticipate and manage risks or oversee multiple insurance policies. Insurers and intermediaries who can help fill that gap by providing innovative, flexible, and affordable product and service options are more likely to fend off emerging competitors for the rather large “small” business market—which generated about 44% of US economic activity as of 2019 and employs nearly half of US workers.

Source: Deloitte

{kind=link}

{kind=link}

{kind=link}