The retrocession market has gained traction in recent years alongside increased investor appetite and an influx of capacity from sources of Alternative Capital.

Alternative Capital increased 410% globally from $19bn in 2008 to over $100bn in 2020, providing reinsurers with the opportunity to cede increasing levels of risks and liabilities to capital market investors via Alternative Risk Transfer, allowing them to optimize their capital management strategies – through Insurance-Linked Securities (ILS), Industry-Loss Warranties, sidecars, collateralized reinsurance deals and more.Alternative Capital is estimated to have provided up to 80% of capacity for the retrocession market.

Natural Disasters, Covid and a Hardening Market

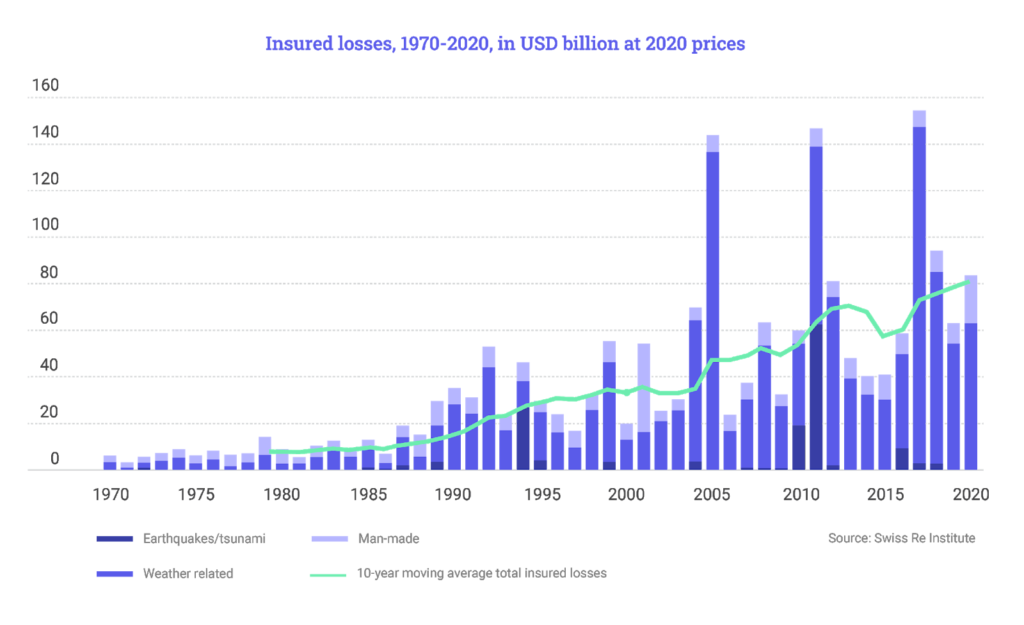

This trend has taken hit after hit beginning with large loss events in 2017 due to large-scale natural disasters such as Hurricane Irma and continued claims deterioration in the following years, leading to disappointing returns and large volumes of trapped capital.

In addition to these, concerns over climate change, increased frequency of natural disasters, and potential Covid-19 losses, have led to a hard market environment, steep increases in premium prices in the last 4 subsequent years and reduced investor appetite. In response, the retrocession market has contracted to levels not seen since 2013.

Is Non-CAT Retrocession the Solution?

Despite the contraction in the retrocession market in recent years due to CAT losses, Alternative Capital availability and investor appetite are at a peak point due to the low interest rate environment. The reinsurance market remains a very attractive option for capital market investors to deploy their capital. According to Willis Re, long-term interest in ILS, particularly from pension funds wanting to diversify their portfolios, remains robust.

The ILS market is increasingly expanding into diverse perils from the Life and non-CAT P&C insurance sectors, both short and long-tailed, transferring a wide range of risks to capital market investors – from motor liabilities and business interruption to longevity and mortality risks.

These Investors are looking for more attractive risk/return and strong diversification points for their portfolio without the looming risk of large-scale natural disasters in the NAT-CAT domain. Also, similarly to CAT, these perils are uncorrelated to the equity markets, and as industry standards for these perils form, investor appetite grows.

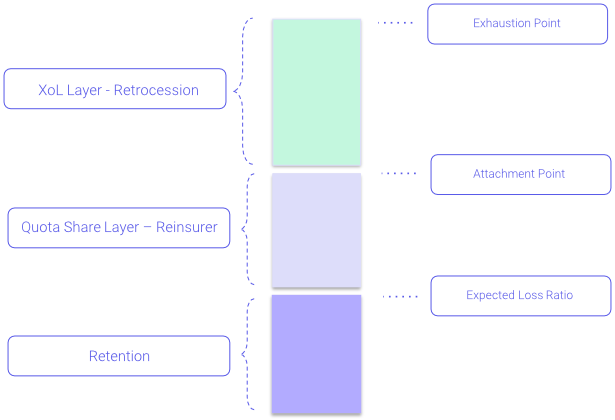

As capacity in the non-CAT ILS market increases, reinsurers are looking to enter retrocession deals for these perils as well – either as a supplement to existing sidecars or other financial vehicles, or to substitute previous traditional reinsurance deals. This allows reinsurers to continue to utilize retrocession for capital optimization, limit downside potential and control loss ratio margin, while earning fee income in the process.

Leveraging AI and ML technologies for Long-Tail Risk Transfer

The appetite for non-CAT retrocession is growing, challenging the industry to more accurately assess long tailed risks.

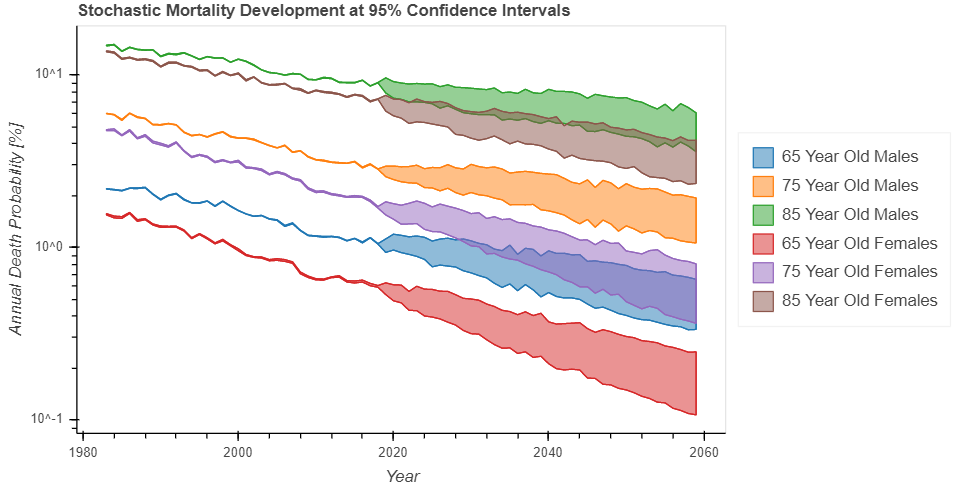

Longevity or mortality risks are the extreme example – they can have ~40-year tails, making it extremely difficult to accurately model and forecast risk development. Utilizing artificial intelligence and machine learning to assess and model risk development over time can greatly improve attachment point forecasting accuracy, allowing the industry to more easily approach these perils and move further into the tail, lowering the price for both sides.

Shorter tailed risks, such as commercial trucking liabilities or event cancellation, can also benefit from the increased accuracy provided by AI-based risk assessment, in addition to faster time-to-market due to process automation.

Better assessment of perils for retrocession deals in the non-CAT insurance domains using artificial intelligence can increase retrocession market capacity allowing for a renewed influx of Alternative Capital, renewing investor appetite while reducing the cost of retrocession for reinsurers, removing more exposure off the balance sheet per dollar spent.

Contact us for more information on Vesttoo’s portfolio-specific AI-based retrocession solutions.

About Vesttoo

Vesttoo specializes in data-driven risk management solutions for the P&C and L&P markets, using cutting-edge technologies to transfer general insurance, lapse, mortality and longevity risk to the capital markets. The company provides insurers and pension funds with affordable, strategic risk transfer to the capital markets, while investors benefit from uncorrelated, high-yield investments with remote loss possibilities.

Vesttoo’s advanced risk-modeling technology transforms the way securities are structured, offered, and traded, providing an accessible, flexible, scalable, and affordable streamlined alternative or supplement to traditional reinsurance.

Learn more here